NIO Reports 20.8K February Deliveries as 58% YoY Growth Masks Brand-Level Weakness

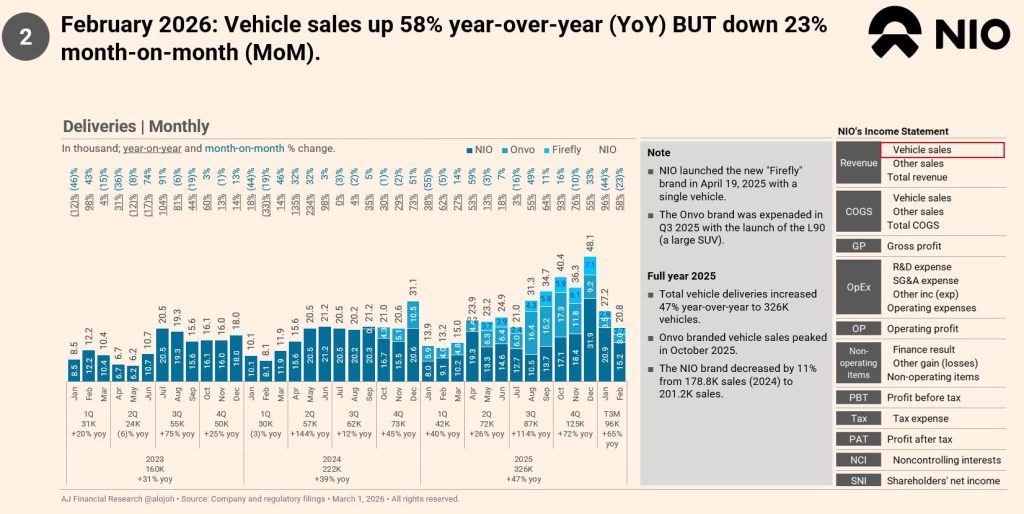

NIO reported 20,800 vehicle deliveries in February 2026, representing a 58% increase compared to the same month last year. While the headline figure signals continued expansion in China’s competitive EV market, a closer look at the data reveals widening performance gaps across the company’s brand portfolio.

On a sequential basis, deliveries declined 23% versus January, highlighting near-term volatility. More importantly, the growth profile appears increasingly concentrated within NIO’s core lineup, while newer brands struggle to scale. This divergence raises strategic questions about whether NIO’s multi-brand expansion is generating the expected synergies.

Key Delivery Results

Overall Performance

- 20.8K vehicles delivered in February 2026

- 58% year-over-year growth

- 23% decline versus January

The strong annual growth reflects improving production execution and stable EV demand in China. However, the monthly contraction suggests that momentum is not evenly distributed across the portfolio.

Onvo Brand Struggles

The brand underperformed expectations in February, with deliveries falling 26% year-over-year despite overall market expansion.

Even when combining January and February to adjust for Lunar New Year seasonality, Onvo sales remain down 35% annually. This decline comes despite new model introductions such as the L90, suggesting that incremental product launches have not yet translated into sustainable demand growth.

Given the supportive backdrop for China’s EV sector, this performance positions Onvo as a structural weak spot within NIO’s broader strategy rather than a temporary fluctuation.

Firefly’s Slow Start

NIO’s newer brand, continues to show limited early traction. Based on the last three months of deliveries, the brand is operating at roughly 50K vehicles annualized, derived from around 12.5K monthly deliveries.

For a recently launched EV sub-brand, this pace indicates gradual adoption rather than breakout acceleration. Without a clearer demand inflection, Firefly risks remaining a marginal contributor to consolidated growth.