Copper Inventories Drop 33,200 Tonnes in First Decline Since October 2024

Global copper inventories have posted their first decline since October 2024, signaling a possible shift in demand dynamics after months of accumulation. A sharp drop in Shanghai warehouse stocks stands out as the main driver, potentially pointing to improving industrial consumption after a recent price correction.

Global Inventories Record First Weekly Decline

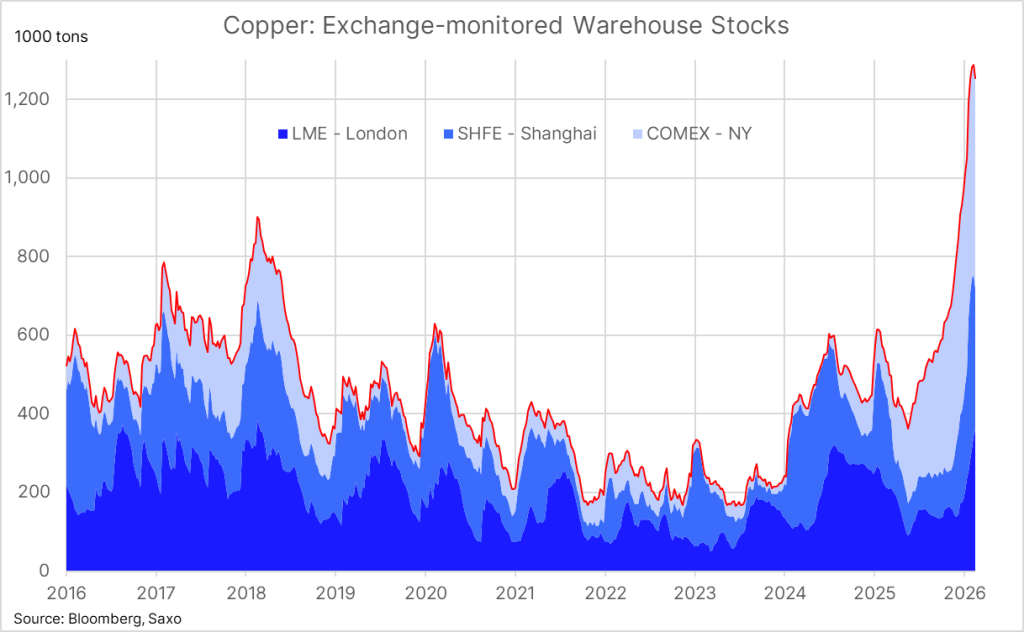

Global copper exchange inventories recorded their first weekly decline since October, falling by 33,200 tonnes to 1.25 million tonnes across major trading venues. The decrease was driven primarily by Shanghai, where stocks dropped by 52,000 tonnes to 359,000 tonnes over two consecutive weeks. This marks a significant 17% decline and may indicate recovering industrial demand following recent market weakness.

Regional data shows mixed developments across exchanges. London Metal Exchange inventories increased by 17,900 tonnes, while COMEX stocks rose by around 1,000 tonnes. However, these increases were more than offset by the sharp drawdown in China as copper continues consolidating within a long term market cycle, as explained in Copper consolidates for 2 months as long-term cycle builds since 2020

The Shanghai decline is particularly important given China’s dominant position in global copper consumption and the metal’s sensitivity to the country’s manufacturing activity.

Price Correction Creates Buying Opportunity

The LME copper benchmark declined about 9% over the past month before the inventory drawdown began. This correction appears to have attracted buyers back into the market as lower prices improved entry conditions.

If demand recovery continues, tightening supply conditions could help support prices in the near term. At the same time, overall inventory levels remain relatively high compared to historical averages, which could limit upside momentum if the drawdown proves temporary.

Copper remains an important barometer of global economic growth. The recent decline in Shanghai inventories may reflect improving industrial activity, while broader macro trends also remain relevant. For example, the copper gold ratio recently dropped to historic lows in 2025 as safe haven demand increased, as discussed in Copper-gold ratio drops to historic lows in 2025 as safe-haven demand surges

This ratio is often used as an indicator of global growth expectations versus market risk aversion.

Demand Recovery Still Faces Risks

Despite the recent inventory decline, risks remain. Stockpiles are still elevated, which could limit price growth if the demand recovery loses momentum.

Copper markets remain highly sensitive to Chinese industrial demand and global manufacturing trends, both of which continue to produce mixed signals. If inventories begin rising again, copper prices could remain in a consolidation phase rather than entering a sustained uptrend.