Central Banks Buy Record Gold Volumes as Price Breaks Historic Highs

Gold has surged to historic highs in 2025 as central banks accelerate bullion purchases at a pace not seen in decades. According to data tracked by the World Gold Council, official sector demand has remained persistently strong, reinforcing the metal’s structural breakout and reshaping global reserve dynamics.

Unlike previous rallies driven by speculative flows, the current move is underpinned by sustained institutional accumulation. Central banks are expanding gold allocations as part of a broader strategy to diversify reserves, reduce reliance on dollar-denominated assets, and hedge against geopolitical and monetary risks.

The breakout in gold prices therefore reflects more than short-term momentum. It signals a structural shift in reserve management strategies across both emerging and developed economies.

Record Central Bank Gold Purchases

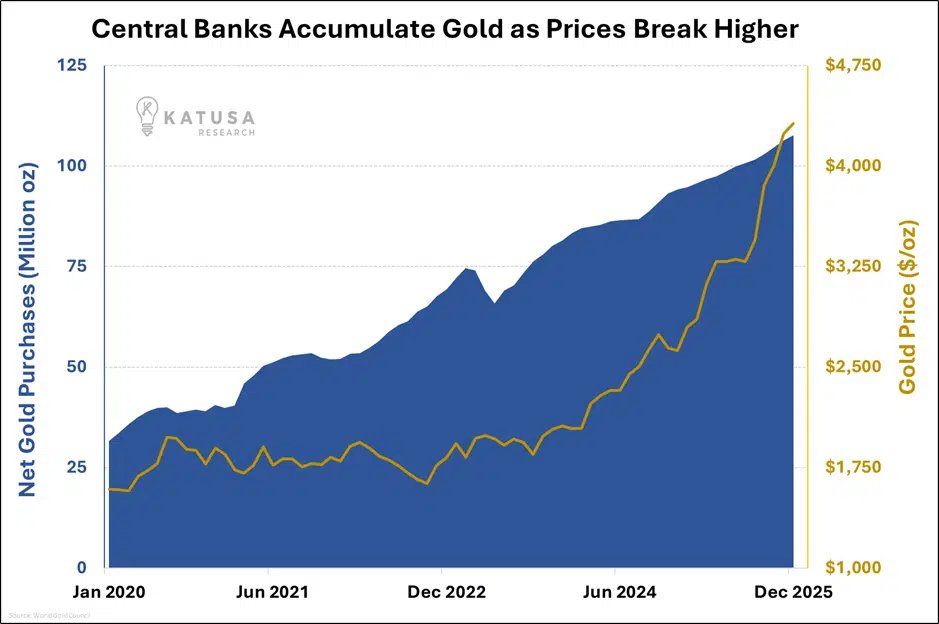

Sustained Buying Since 2020

Net gold purchases by central banks have trended higher since 2020, reaching levels comparable to the post-global financial crisis period. Official data shows that demand remained elevated throughout 2024 and has continued into 2025, reinforcing a multi-year accumulation cycle rather than a temporary surge.

Among the most significant buyers has been the People’s Bank of China, which has reported consecutive monthly increases in gold reserves for more than a year. Other emerging market central banks have followed a similar path, gradually increasing exposure to physical gold as part of broader reserve rebalancing.

This steady accumulation has tightened the structural supply-demand balance, providing durable price support even during episodes of broader market volatility.

Diversification Away from Dollar Assets

The renewed interest in gold reflects a long-term diversification strategy. Several countries are reducing their reliance on traditional reserve assets, including U.S. Department of the Treasury securities, and reallocating capital into hard assets perceived as politically neutral stores of value.

Beyond diversification, gold functions as a hedge against inflation risk, currency debasement, and geopolitical uncertainty. In an environment characterized by elevated global tensions and shifting monetary policy expectations, central banks appear focused on strengthening balance sheet resilience.

The trend suggests policymakers are preparing for increased volatility or structural adjustments within the global monetary system.

Macro Forces Supporting Gold

Geopolitical and Inflation Pressures

In addition to official sector demand, macroeconomic conditions continue to support elevated gold prices. Persistent inflation concerns, rising currency volatility, and geopolitical friction across multiple regions have reinforced the metal’s defensive appeal.

Historically, gold performs as a store of value during systemic stress. The sustained institutional bid has helped absorb downside pressure, stabilizing the market even during broader risk-off episodes.

Institutional Signaling

Market analysts increasingly interpret this coordinated accumulation as strategic repositioning rather than tactical buying. Central banks appear to be redefining gold’s role within reserve frameworks, elevating it from a legacy allocation to a core hedge against systemic and monetary risk.

Such positioning carries signaling power. When central banks adjust reserves at scale, it alters investor perceptions of currency stability, inflation trajectories, and macro risk management.

Why This Matters for Global Markets

When central banks meaningfully expand gold reserves, the impact extends beyond commodity pricing. Sustained official demand influences liquidity conditions, long-term price floors, and investor allocation strategies.

If major economies continue treating gold as a strategic reserve anchor, it reshapes how global markets evaluate safe-haven assets, currency exposure, and macro hedging frameworks.

The current accumulation phase therefore represents not only a price story, but a structural evolution in global reserve management.

Outlook for 2025 and Beyond

If central bank purchases remain elevated, gold may retain structural support even during periods of consolidation. The convergence of institutional demand, geopolitical uncertainty, and currency volatility creates a foundation for sustained price sensitivity with an upward bias.

Short-term corrections remain possible. However, the dominant narrative centers on reserve diversification, monetary uncertainty, and long-term risk mitigation.

Source: Katusa Research